In my article Don’t Chase Yield (February 11, 2021) I recounted advising in 1990 a 60-year-old gentleman from my neighbourhood in Woollahra with $3m to invest. I prepared strategic advice to receive $30,000 per month income; pay no income tax; and grow his wealth to keep pace with inflation.

My neighbour said that he appreciated the advice, but ended up placing his funds into a three-year term deposit that was paying 14% per annum. He would receive annual interest of $420,000, but after paying annual tax of $195,000 (tax rates were a lot higher in the 1990s) his income was reduced to

$18,750 per month.

Unfortunately when the term deposit matured three years later, interest rates had fallen to 4.25% and his after tax income dropped to just $6,200 per month, well below his cost of living.

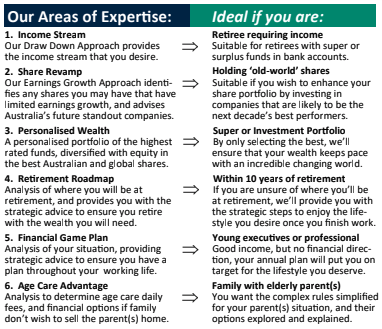

In my article Securing a 6% to 8% Income Stream (February 3, 2021), I explained how, as a result of falling interest rates in the 1990s, I developed the Draw Down Approach to solve the income dilemma facing retirees. My approach has always been ideal for clients drawing monthly tax-free income from their superannuation funds, but we have also seen the approach become very popular with people of the Wentworth electorate who have surplus funds in bank accounts earning very little interest. If you too have surplus funds in bank accounts, please come in and meet with me to discuss how our draw down approach can provide you with your desired income stream, without taking huge risks with your wealth. Your initial meeting with me will be provided without cost or obligation.

Disclaimer: This information is general advice only, & has been prepared without taking into account the objectives, financial situation, or needs of any individual. It is not a specific recommendation to buy, sell or hold any product or security. Readers should seek financial advice before making a decision & should consider the appropriateness of this advice in light of their own objectives, financial situation, &needs.